Key Takeaways

- Poor account reconciliation exposes law firms to bar complaints, malpractice claims, and trust account violations that can end careers.

- Law firms managing IOLTA or client trust accounts are legally required to reconcile those accounts ,not just as good practice, but as an ethical obligation under ABA Model Rule 1.15.

- Automating the account reconciliation process can cut processing time by up to 90%, giving your attorneys and staff more billable hours back.

- Virtual accounting staff trained in legal billing can handle your reconciliation workflows at a fraction of the cost of a full-time hire, without the compliance risk of doing it in-house with untrained staff.

Let's Be Honest: Most Law Firms Are Flying Blind on Their Finances

You didn't go to law school to reconcile bank statements. But here's the uncomfortable truth: if your firm's accounts aren't being reconciled consistently and correctly, you're sitting on a ticking time bomb.

We're not being dramatic. The American Bar Association consistently identifies trust account mismanagement, often rooted in poor reconciliation as one of the leading causes of attorney disciplinary actions across the country. One overlooked discrepancy in an IOLTA account can trigger a bar investigation, even if the error was completely unintentional.

So whether you're a solo practitioner or managing a multi-partner firm, this guide is written specifically for you to help you understand what account reconciliation really means in a legal context, why maintaining accurate financial records isn't optional, and how to stop treating it like an afterthought.

What Is Account Reconciliation for Law Firms?

Account reconciliation refers to the accounting process of comparing two sets of financial records to confirm they are accurate, consistent, and complete. Simply put, you're verifying that your internal records match what your external bank statement, credit card statements, or vendor invoices actually show.

For law firms, this goes well beyond standard business bookkeeping. Your finance team isn't just reconciling a single checking account they're managing:

- Operating accounts — your firm's day-to-day cash flow, expenses, and revenue

- Client trust accounts (IOLTA) — funds that legally belong to your clients, not your firm

- Accounts payable — vendor invoices, court fees, expert witness payments

- Accounts receivable — outstanding client invoices and retainer balances

- Payroll accounts — attorney salaries, paralegal wages, contractor payments

- Credit card accounts — firm expenses tracked against credit card statements

Each of these carries its own reconciliation requirements and in the case of trust accounts, its own ethical and legal obligations under your state bar's rules of professional conduct. When your accounting teams fail to reconcile accounts consistently, the consequences compound quickly.

Why Law Firms Can't Treat the Reconciliation Process Casually

Here's what's actually at stake when reconciliation falls through the cracks at a law firm.

Trust Account Violations Are Career-Ending

Every state bar has specific rules governing client trust accounts. Most follow ABA Model Rule 1.15, which requires lawyers to keep client funds separate from firm funds, maintain complete accounting ledgers, and produce accurate financial records on demand. Failure to perform account reconciliation on those accounts even due to negligence rather than intent can result in:

- Suspension or disbarment

- Mandatory restitution to clients

- Civil malpractice liability

- Criminal charges in cases involving misappropriation

The ABA Standing Committee on Ethics and Professional Responsibility has repeatedly emphasized that not knowing about a discrepancy is not a defense. Regular account reconciliation matters precisely because it gives you visibility before a problem escalates.

Financial Fraud Hits Law Firms Hard

According to the ACFE's 2022 Report to the Nations, professional services firms including law practices experience a median fraud loss of $200,000 per incident. Unauthorized transactions, billing fraud, expense manipulation, and unauthorized disbursements are all significantly more likely when internal controls around reconciliation are weak or absent. Regularly reconciling accounts is one of the most effective anti-fraud controls your firm can implement.

Inaccurate Financial Statements Create Real Legal Exposure

When your company's general ledger doesn't reflect reality, every financial decision you make staffing, expansion, partner distributions is based on bad data. Worse, inaccurate financial statements handed to lenders, auditors, or tax authorities create liability that goes far beyond an accounting headache.

You're Also an Audit Target

Law firms that handle large settlements, government contracts, or regulated industries often face audits from the IRS, state bar, or client auditors. Unreconciled accounts during an audit signal poor internal controls, which can escalate a routine review into something far more serious. Your source documents, journal entries, and reconciliation records are the first things an auditor will ask for.

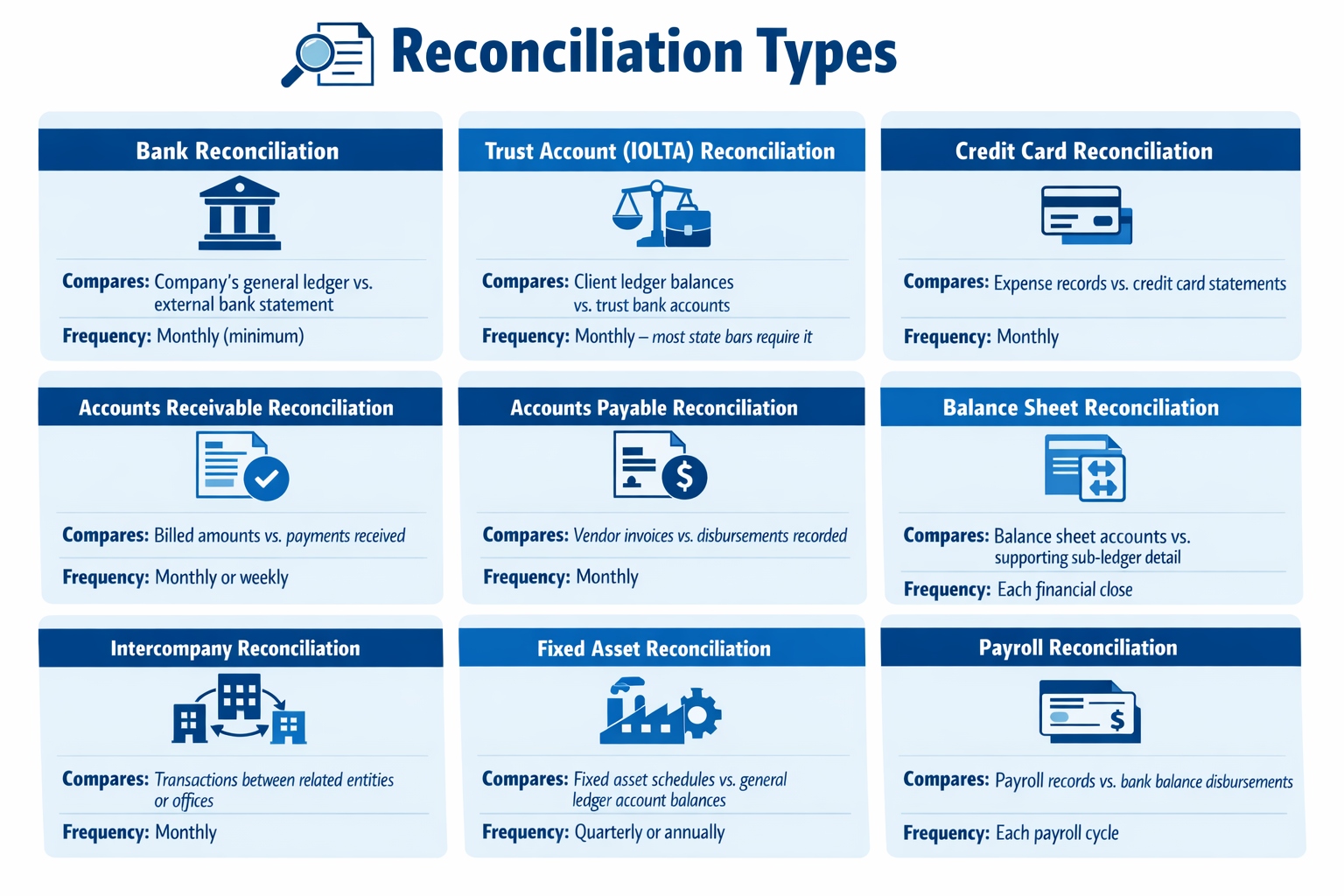

Types of Account Reconciliation Every Law Firm Needs to Understand

Not all reconciliation carries the same weight but all of it matters. Here are the primary types of account reconciliation your firm should be running consistently across each accounting period.

A critical note on trust account reconciliation: Most state bars require what's called a three-way reconciliation comparing the external bank statement, the trust account ledger, and individual client subsidiary ledgers simultaneously. If those three records don't agree, you have a problem that needs immediate resolution. This is not a reconciliation process you can shortcut.

How the Account Reconciliation Process Actually Works at a Law Firm

Let's walk through it practically, the way it should actually be done step by step, each accounting period, without exception.

Step 1 Gather Your Source Documents

Pull your bank statements, general ledger account reports, client ledger detail, credit card statements, vendor invoices, and any prior reconciliation records. If you're using legal accounting software like Clio, LEAP, or CosmoLex, most of this lives in the system already. Completeness here prevents rework later.

Step 2 Establish Your Beginning Balance

Before you start matching transactions, confirm your beginning balance. Your internal records and your external bank statement should agree on the opening figure for the period. If they don't, a discrepancy from a prior accounting period hasn't been resolved and that's problem one.

Step 3 Compare Internal Records Against External Statements

Match each transaction in your general ledger account against your bank statement or credit card statements line by line. In legal billing, this means verifying every trust deposit, every disbursement, every retainer draw, every bank fee. Your accounting teams should be cross-referencing transaction details dates, amounts, payees not just totals.

Step 4 Identify Discrepancies and Missing Transactions

Flag anything that doesn't match. This includes missing transactions that appear in one record but not the other, amount differences, duplicate entries, or unrecorded bank fees. In a law firm context, pay particular attention to trust account entries a missing transaction in a client ledger is both an accounting problem and a potential ethics issue.

Step 5 Investigate and Post Journal Entries

Don't just fix the number understand why it was wrong. Post correcting journal entries for genuine data entry errors. Document timing differences such as outstanding checks separately those aren't errors, they're legitimate timing gaps that will clear in the next period. If something resembles unauthorized transactions, escalate immediately.

Step 6 Reconcile Accounts and Confirm the Account Balance

After adjustments, your adjusted account balance in the general ledger should match your external bank statement. For trust accounts, all three records bank statement, trust ledger, and individual client balances must agree. If they do, the reconciliation is complete. If they don't, return to step four.

Step 7 Document Findings Thoroughly

In a law firm, documentation isn't optional. Your reconciliation records need to clearly show who prepared them, when, what discrepancies were found, how they were resolved, and what journal entries were posted. This is your evidence of compliance and your first line of defense if a bar complaint or audit ever arrives.

Step 8 Enforce Segregation of Duties on Review

The person who prepares the reconciliation should not be the only person who reviews it. Segregation of duties is a fundamental internal control and for trust accounts especially, it is non-negotiable. A managing partner, controller, or outsourced accounting professional should sign off before you file.

Step 9 File, Report, and Retain

Store completed reconciliations with all supporting documents for the retention period your state requires typically five to seven years. Some state bars specify longer retention for trust account records. Report any material findings to firm leadership and include relevant adjustments in your financial statements before the financial close.

Account Reconciliation Discrepancies: What Causes Them at Law Firms

Understanding the root causes of account reconciliation discrepancies makes your team faster at resolving them and better at preventing them.

Data Entry Errors and Manual Data Entry

Human error in manual data entry is the single most common source of discrepancies across accounting teams of every size. A transposed number, a decimal in the wrong place, or a payment applied to the wrong client matter can throw off an entire account. This is exactly why relying solely on manual data entry for a high-volume legal practice is a risk most firms shouldn't take.

Timing Differences

Outstanding checks, deposits in transit, or electronic transfers processed after the statement date create legitimate differences between your internal financial records and your external bank statement. These aren't errors but they need to be clearly documented during the reconciliation process so reviewers understand why the balances temporarily differ.

Bank Fees and Unrecorded Charges

Bank fees applied directly to your bank accounts mid-period often don't make it into the general ledger until someone catches them during reconciliation. The same applies to interest credits, wire transfer fees, and merchant processing charges.

Duplicate Payments or Invoices

In firms with high transaction volume and multiple staff handling accounts payable, duplicate payments to vendors are surprisingly common. A consistent vendor reconciliation process catches these before they become billing disputes.

Unauthorized Transactions

Any transaction that wasn't properly authorized whether from fraud, unauthorized system access, or a staff member exceeding their authority will surface as a discrepancy during reconciliation. This is precisely why regular account reconciliation matters as a fraud detection control, not just a bookkeeping exercise.

Integration Failures Between Accounting Software

When your practice management platform, billing software, and accounting software don't sync cleanly, gaps in financial records emerge. Transactions recorded in one system may not transfer correctly to another, creating discrepancies that are easy to miss if reconciliation isn't performed consistently.

Misapplied Retainer Draws

In legal billing specifically, retainer draws applied to the wrong client matter or recorded at the wrong amount are a common source of trust account discrepancies and potentially a bar compliance issue.

Best Practices for Law Firm Account Reconciliation

Here's what the firms that get this right consistently do differently.

Reconcile accounts consistently every month no exceptions. Many state bars require it for trust accounts. For operating accounts and accounts receivable, monthly reconciliation is the floor, not the ceiling. High-volume credit card accounts should be reviewed weekly.

Use legal-specific accounting software. Generic tools require significant customization to handle client-level trust ledger tracking. Purpose-built platforms handle the full reconciliation process including three-way trust reconciliation natively. More on the right tools shortly.

Separate duties between preparer and reviewer. Segregation of duties is both a best practice and an internal control requirement. The bookkeeper reconciles; the managing partner or controller approves. Never the same person performing both functions.

Keep client trust ledgers current in real time. Waiting until month-end to post trust transactions creates a backlog that increases the risk of data entry mistakes and missing transactions during reconciliation.

Set a fixed financial close date each month. Reconciliation discipline starts with a non-negotiable schedule. When it's optional or "whenever there's time," it doesn't happen reliably.

Document every discrepancy, even small ones. A $10 unexplained difference is still an unexplained difference. Resolve it, document it, and move on but never skip it because it seems trivial. Patterns in small discrepancies are often early warning signs of larger problems.

Maintain robust source documents. Every journal entry, every adjustment, every corrected data entry mistake should be traceable back to a source document. This is your audit trail and your compliance record.

Train everyone who touches financial records. Paralegals managing billing, office managers handling deposits, and any staff with access to your accounting software all need to understand their role in maintaining accurate financial records.

Perform balance sheet reconciliation at every financial close. Balance sheet accounts including liabilities and long-term assets need to be reconciled each period, not just bank accounts. A complete balance sheet reconciliation ensures your financial statements reflect reality before they're finalized.

Common Reconciliation Mistakes Law Firms Make

Even well-run firms get tripped up by these:

- Reconciling trust accounts only when a bar audit is coming — by then, discrepancies have compounded and the damage is done

- Letting the same person record and reconcile transactions — this removes the safeguard that catches both data entry mistakes and intentional misconduct

- Mixing client funds with firm operating funds — even temporarily, this constitutes commingling under ABA Model Rule 1.15, regardless of intent

- Relying on bank balance alone — trust account compliance requires a full three-way reconciliation, not just a bank-to-ledger check

- Using generic bookkeeping tools — software not designed for legal accounting may not support client-level trust ledger tracking or produce compliance-grade financial records

- Skipping balance sheet reconciliation entirely — many firms reconcile their bank accounts diligently but neglect balance sheet accounts altogether

Manual vs. Automated Accounts Reconciliation — What Makes Sense for Your Firm?

A Gartner study found that finance automation reduces reconciliation processing time by up to 90%. For a firm billing hundreds of hours per month across multiple attorneys, that's not a marginal gain it translates directly into recovered billable time and reduced overtime for your administrative staff.

That said, automated accounts reconciliation doesn't eliminate the need for human oversight. Someone still needs to investigate exceptions, approve completed reconciliations, and ensure your accounting software is correctly configured for your state's trust account rules. Automation handles the matching transactions work; your team handles the judgment calls.

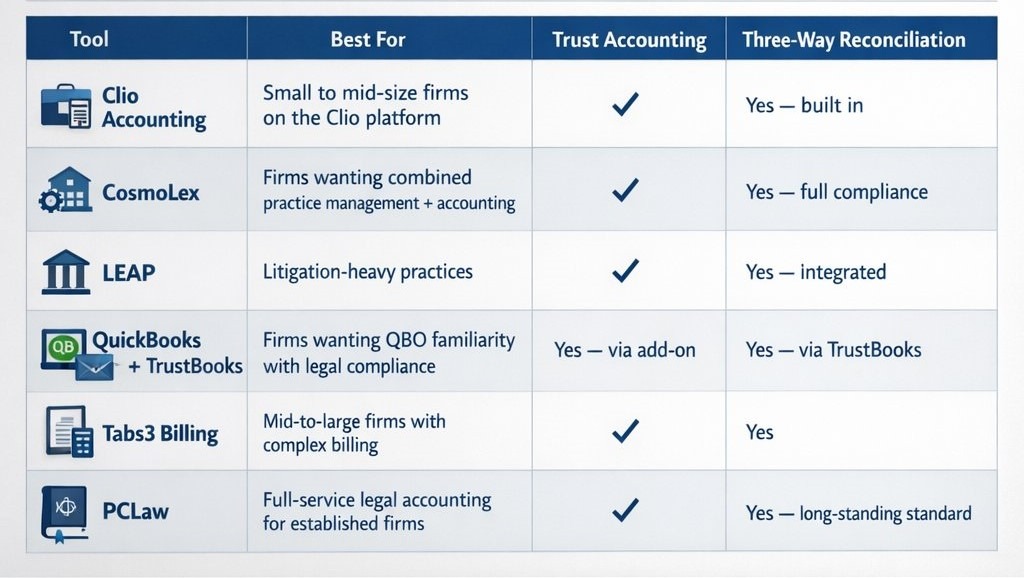

The Right Accounting Software for Law Firm Reconciliation

Choosing the right tool makes a significant difference not just in efficiency, but in your ability to meet compliance obligations and manage cash flow effectively. Here's how the leading options compare for law firms specifically.

If your firm is currently using a general accounting tool with no legal-specific features, the key question to ask is: can it produce a compliant three-way trust account reconciliation? If the answer is no or "we're not sure" your compliance exposure is real and worth addressing now rather than during an audit.

📚 Also Read: Best Legal Case Management Software in 2026: What Law Firms Need to Know

Your Firm Deserves a Smarter Way to Handle This

Account reconciliation isn't glamorous work but for a law firm, it's mission-critical. It protects your license, your clients' funds, your financial health, and everything you've built. The firms that stay out of trouble aren't necessarily the ones with the biggest finance teams. They're the ones that treat the reconciliation process as a non-negotiable part of running a professional practice, with the right accounting software, consistent internal controls, and qualified people reviewing the numbers every single month.

The good news? You don't have to do it yourself. Legal Intaker's virtual staffing solutions connect law firms with skilled virtual accounting professionals who understand the specific demands of legal bookkeeping including trust account compliance, three-way reconciliation, client ledger management, and the documentation standards your state bar requires. Our virtual staff integrate directly with your existing accounting software, follow your firm's internal controls, and deliver reconciliation work that's clean, compliant, and audit-ready every month without the overhead of a full-time salary, benefits, or office space.

If your firm is still handling reconciliation manually, inconsistently, or not at all let's fix that today. Schedule a consultation with LegalIntaker and find out how a dedicated virtual accounting professional can protect your firm's financial health starting this month.

FAQs About Account Reconciliation

1. How often does a law firm need to reconcile its trust account?

Most state bars require trust account reconciliation at least monthly, aligned with your bank statement cycle. The ABA recommends a three-way reconciliation comparing your bank statement, trust account ledger, and individual client balances every single month. High-volume trust accounts may warrant more frequent review. Check your state bar's specific rules, as requirements vary.

2. What happens if a law firm's trust account reconciliation doesn't balance?

Stop, and investigate immediately. An unbalanced trust account means either a recording error in your financial records or in the worst case a compliance violation. Do not wait to resolve it. Document your investigation, identify the source of the discrepancy, post the correcting journal entries, and record the resolution clearly. If the difference is unexplained and material, contact your state bar's ethics hotline before the situation escalates.

3. Can a law firm use QuickBooks for trust account reconciliation?

QuickBooks can be used, but it requires careful configuration and ideally a legal-specific integration like TrustBooks to handle client-level trust ledger tracking. Out of the box, standard QuickBooks is not designed for legal trust accounting compliance and won't automatically produce a three-way reconciliation. Many malpractice carriers and state bars advise using purpose-built legal accounting software to maintain the accurate financial records your bar rules require.

4. Who should be responsible for account reconciliation at a law firm?

A trained bookkeeper or legal accountant should prepare the reconciliation each accounting period. A partner, controller, or office manager should independently review and approve it. The person handling trust fund transactions should never be the sole reviewer of trust account reconciliations segregation of duties between the preparer and approver is a basic internal control that every firm should follow, regardless of size or transaction volume.

.webp)

.webp)

.webp)

.webp)